When it comes to investing in shares, it’s often said that time is your friend.

Data shows that investing small amounts consistently over time and riding out the ups and downs of the market by holding onto your investments for the long-term, can produce a healthy return.

Over the past two decades, the top 500 US companies averaged a 10% annual return and Australia’s S&P ASX All Ordinaries Index recorded an average annual return of 9.2%.i

Those returns have been delivered despite some catastrophic events that sent the markets plummeting including the dot-com bubble crash, the Global Financial Crisis, and the effects of Covid-19.

It takes grit to hold on as the markets plummet, but the best way might be to avoid the hype and tune out the ‘noise’. It can be a trap checking prices every day and week, causing heightened stress and anxiety about your portfolio, a recent example being this week’s ‘Japan Trade’ or the mid-2024 Microsoft outage, which briefly impacted investor confidence. At Clear Sky, our advisers can help you maintain a longer-term view, so if you ever have concerns, please feel free to give us a call.

The seasonal cycle of markets:

The cycle of endless phases of good and bad times are a constant for markets, says AMP’s Chief Economist and Head of Investment Strategy Dr Shane Oliver.ii

“Some relate to the three-to-five-year business cycle, and many of these are related to the crises that come roughly every three years. Some cycles are longer, with secular swings over 10 to 20 years in shares,” he says.

Most cycles follow a pattern of early upswing, after the market has bottomed out followed by the bull market, when investor confidence is strong, and prices are rising faster than average. Then the market hits its peak as prices level out before negative investor sentiment drives a bear market. Finally, the bottom of the cycle is reached as prices are at their lowest.

There are also certain seasonal market cycles that may be helpful in buying and selling decisions. Note, though, that there are always exceptions. The much-quoted rule, “past performance is not an indication of future performance” is always important to keep in mind.

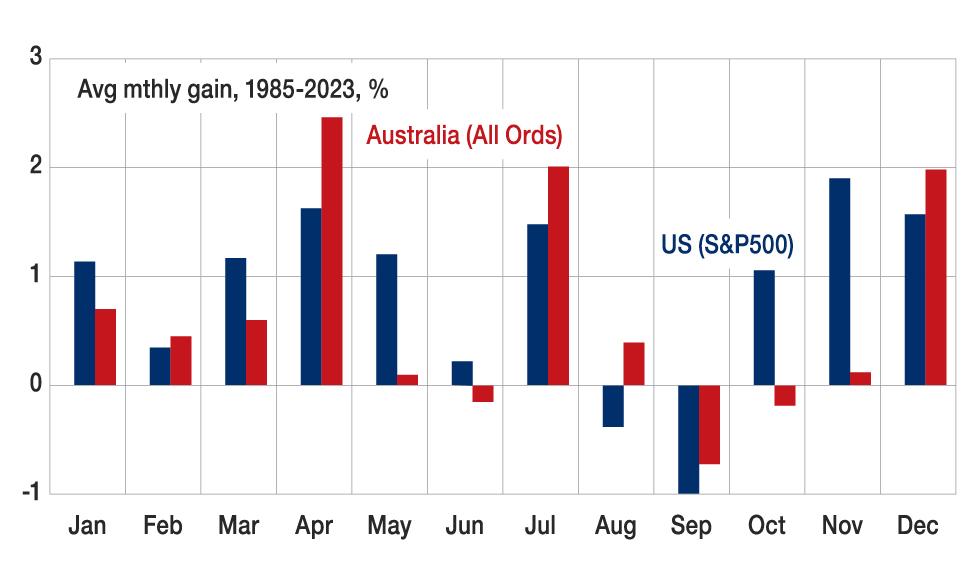

As the graph shows, April, July and December have tended to be the strongest months of the year.

Since 1985, the ASX All Ordinaries Index has seen gains in April averaging 2.4%, with July averaging 2% and December 1.9%, which compares to an average monthly gain for all months of 0.62%. But these patterns have weakened a little over time, with lower average gains in April, July, and December more recently.iii

The seasonal pattern in shares:

Source: Bloomberg, AMP

Note: Data is based on the ASX All Ordinaries Index, which includes about 500 of the largest listed companies.

By contrast, S&P ASX 200 monthly returns from 1993 to 2020 found April, October, and December to be the strongest months, according to 2021 UBS research.iv The research from both indices shows June to be the worst month for performance, often because investors sell before the end of the financial year to reduce their tax bill – a strategy known as tax-loss selling. Investments that have incurred capital losses are sold to offset any capital gains to potentially reduce taxable income.

“In the United States, the markets have usually been relatively weak in the September quarter, strengthened into the New Year and remained solid to around May or July,” says Oliver.

November and April have been the strongest months for US shares for the past 30 years, with average monthly gains of 1.9% and 1.6% respectively.

The Magnificent Seven:

Despite the rise and rise of seven US technology stocks in the past 18 months, known as The Magnificent 7, their price pattern has, more-or-less, followed these seasonal cycles.

The seven stocks – Nvidia, Alphabet, Microsoft, Apple, Meta, Amazon, and Tesla – returned more than 106% in 2023 alone.v

In the first half of 2024, their prices rose around 33% on the US S&P 500 index while the rest of the index increased by only 5%. Last year’s numbers were even more stark: the Magnificent 7 rose 76% while the rest of the index increased just 8%.vi

During this period the S&P ASX 200 has risen by about 2%.

But another story has been emerging in recent months. The Magnificent 7 has now become the Magnificent 3, thanks to intense excitement around artificial intelligence (AI). Nvidia, Alphabet and Microsoft leapt into the lead on the index, doubling the performance of the other four.vii

Of the seven stellar performers, Nvidia has been the market darling, with its price almost tripling in 12 months. But as is often the way with rapid stock price movements, a correction followed, which has seen Nvidia’s value plunge $646 billion. It has since managed to claw back some of the lost territory and is still worth more than US$3 trillion. This correction knocked the company from the biggest in the world, a title it held briefly before the plunge, to number three after Microsoft and Apple.

The performance of Nvidia and the Magnificent 7 is a real-time lesson in market dynamics and cycles.

Some describe the activity as a bubble that is due to burst at some time in the future. Others say the Magnificent 7 stocks are undervalued and have further to go.

Please get in touch if you’d like to review and discuss your investment portfolio. We can help you understand what you’re investing in and the potential risks, as well as help you stay focussed on your long-term investing goals.

i 2023 Vanguard Index Chart: The real value of time – Vanguard

ii The 9 most important things I have learned about investing over 40 years – AMP

iii The ’best’ and the ‘worst’ months for shares – asx.com.au

iv CHART: The months of the year when the ASX performs best – and why – Stockhead

v The magnificent 7: A cautionary investment tale – Vanguard

vi Guide to the Markets – J.P. Morgan Asset Management

vii The Kohler Report – ABC News

Information contained in this document is considered to be true and correct at time of publication. In addition, the information provided is general information only, and does not take into account any individuals’ objectives, financial situation and needs. Before acting on any information contained herein, you should consider the appropriateness of the advice having regard to your personal objectives, financial situation and needs.